Form 1099 reporting can look like a simple tax task. But it also reveals how the company pays people, classifies workers, documents vendors, and manages compliance risk.

In 2026 because 1099 reporting continues to change. The IRS 2026 General Instructions for Certain Information Returns include updates involving address fields, Forms 1099-MISC, 1099-NEC, 1099-K, cash tips, overtime compensation, and other reporting details.

For business owners, finance teams, payroll departments, bookkeepers, and compliance officers should aim to file correctly, keep clean records, and avoid reporting gaps that can become tax, employment, or legal problems.

Why 1099 reporting requirements matter

A Form 1099 usually reports certain payments made outside regular payroll. That may include payments to independent contractors, vendors, attorneys, platforms, and digital asset brokers, depending on the form and the transaction.

In our work with business owners, these problems often appear late in the year. A company may discover that W-9s were never collected, taxpayer identification numbers do not match IRS records, a contractor has been working more like an employee, or payments were made from the wrong entity.

By then, the issue is harder to fix.

This is why you should review your 1099 compliance before filing season. A clean process starts when your business hires a contractor, onboards a vendor, signs an agreement, opens a new LLC, or receives payments through a platform.

What changed for 1099 reporting in 2026?

The IRS says that, for forms revised in 2026, address fields were separated into individual entry boxes. Forms 1099-MISC and 1099-NEC were updated to allow reporting of cash tips, Treasury Tipped Occupation Code, and overtime compensation. Form 1099-K was also updated to allow reporting of cash tips and the applicable Treasury Tipped Occupation Code.

Businesses should also pay attention to Form 1099-DA, which is used to report digital asset proceeds from broker transactions. The IRS states that Form 1099-DA is used for digital asset proceeds, and IRS instructions address reporting for sales of digital assets after 2025.

These updates will not affect every company in the same way. A consulting firm, marketplace seller, law firm, crypto-related business, real estate operator, and company with many contractors may each have different reporting risks.

1099-NEC and nonemployee compensation

Form 1099-NEC is commonly used for nonemployee compensation. Businesses may need to file Form 1099-NEC when they pay independent contractors for services performed for a trade or business.

This often includes freelancers, consultants, service providers, and other nonemployees.

Before issuing a 1099-NEC, you should review whether the person was actually an independent contractor. The form reports a payment. It does not prove the worker was classified correctly.

A basic review should include:

- the written agreement;

- the type of work performed;

- who controlled the schedule and methods;

- whether the worker had business independence;

- whether a valid Form W-9 was collected;

- whether payments match the company’s books.

After determining someone is an independent contractor, the first step is to have the contractor complete Form W-9, which requests the correct name and taxpayer identification number. Remember, the W-9 should be kept in the company’s files for four years.

Contractor or employee? Classification matters

This is one of the biggest risks behind 1099 reporting.

Your business cannot make someone an independent contractor just by issuing a 1099. The IRS looks at the actual relationship. It considers the degree of control and independence, including behavioral control, financial control, and the relationship between the parties.

There is no single factor that automatically makes someone an employee or an independent contractor. You must look at the entire relationship and document the factors used in the decision.

| Issue | 1099 contractor | Employee |

|---|---|---|

| Payment reporting | Usually Form 1099-NEC | Usually Form W-2 |

| Control | More independence | More business control |

| Taxes | Self-employment tax may apply | Payroll withholding usually applies |

| Risk area | Misclassification, W-9, contract terms | Payroll taxes, benefits, wage rules |

| Key review | Actual work relationship | Employer obligations |

If the company controls how the person works, provides tools, sets the schedule, and treats the worker like staff, the relationship may need a closer review.

1099-MISC, attorney fees, and vendor payments

Form 1099-MISC still matters for many business payments. Depending on the facts, it may apply to categories such as rents, prizes and awards, certain medical payments, and other miscellaneous payments. IRS instructions also include rules for certain attorney fee reporting.

Attorney payments deserve attention because reporting can depend on the type of payment, who received it, and how the payment was made. Vendor payments can create similar confusion.

A business should be able to explain why a payment was reported on 1099-MISC, 1099-NEC, 1099-K, another form, or not reported at all. That explanation depends on records, not memory.

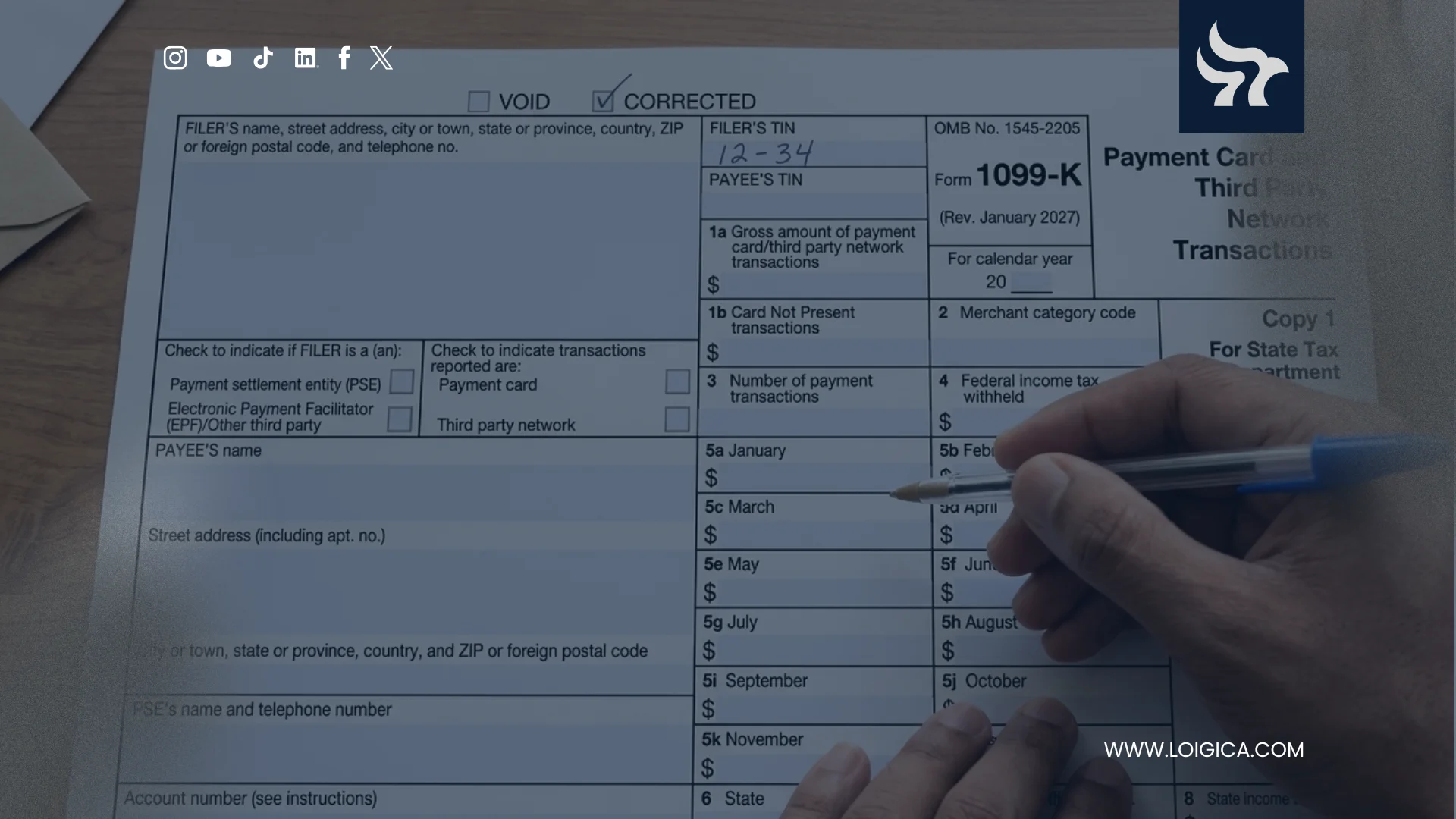

1099-K and third-party payment platforms

Form 1099-K applies to certain payment card and third-party network transactions.

If your business receives payments through platforms, marketplaces, apps, or payment processors, you should take a closer look. A 1099-K may not match net revenue because it can reflect gross payments before refunds, platform fees, chargebacks, or other adjustments.

The business still needs clean books. It should reconcile 1099-K amounts with sales records, refunds, fees, taxes, and business income.

This is especially important for companies using multiple payment platforms or mixing personal and business transactions.

1099-DA and digital asset reporting

Form 1099-DA is a major development for businesses and taxpayers involved with digital assets.

Form 1099-DA is used to report digital asset proceeds from broker transactions. The form instructions state that, for 2026 and beyond, reporting includes mandatory gross proceeds reporting for digital assets and basis information for covered securities.

Businesses that receive, sell, exchange, or hold digital assets should review their records early. A 1099-DA may not tell the full story. The company may still need information about basis, proceeds, wallets, transfers, business purpose, and accounting treatment.

This is relevant if your company uses crypto payments, holds digital assets, operates in Web3, or has founders moving assets between personal and business accounts.

IRS TIN matching, W-9s, and backup withholding

TIN matching can help your business reduce filing errors before forms are submitted.

TIN Matching allows a payer or authorized agent to match taxpayer identification number and name combinations with IRS records before submitting certain information returns, including Forms 1099-DA, 1099-K, 1099-MISC, and 1099-NEC.

Backup withholding can also become an issue when payee information is missing or incorrect. The IRS notes that payers of income reported on several 1099 forms may use the TIN Matching program to validate TIN and name combinations before filing.

A practical process usually includes collecting W-9s before payment, validating vendor information, assigning internal responsibility, and responding quickly to mismatch notices.

Common 1099 compliance gaps

In our work with business clients, we have seen that 1099 problems often show up late, when the company is already preparing year-end filings.

By that point, the issue is usually not just one missing form. The business may discover that some contractors were paid before collecting W-9s, that a vendor’s taxpayer identification number does not match IRS records, or that someone treated as a contractor was actually working under conditions closer to an employee relationship.

We also see problems when companies grow into more complex structures. For example, a business may have more than one LLC, but payments, contracts, invoices, and bank accounts are not clearly separated. In those cases, 1099 reporting can expose records that do not match the way the company is supposed to operate.

Common issues include:

- paying contractors before collecting W-9s;

- using contractor agreements without reviewing the actual work relationship;

- mixing personal and business payments;

- paying vendors from the wrong entity;

- overlooking attorney fee reporting rules;

- failing to reconcile 1099-K forms;

- treating digital asset transactions casually;

- using several LLCs without clean books, contracts, and bank accounts.

These mistakes are not always intentional. Many times, the company simply grew faster than its internal systems. But once reporting season arrives, weak records can create questions about worker classification, vendor documentation, corporate separateness, and liability protection.

Loigica can help business owners review legal structure, contractor relationships, vendor documentation, and compliance risks before reporting issues become larger problems. Contact us here.

What businesses should review before year-end

From what we see with business clients, the companies that handle 1099 reporting better are usually not the ones that wait until January to organize everything. They review the process earlier, while there is still time to fix records, request missing documents, and clarify how payments were made.

Before filing season, your business should review all the 1099 reporting requirements, such as:

- contractor and employee classification;

- vendor onboarding;

- W-9 collection;

- TIN matching;

- payment methods;

- 1099-NEC vs 1099-MISC decisions;

- 1099-K reconciliation;

- digital asset transactions;

- attorney fee payments;

- backup withholding exposure;

- coordination between payroll, AP, tax, legal, and compliance.

In our experience, this review is most useful when it reflects how the company actually operates. If contractors are managed like employees, if vendors are paid from different entities, or if payment records do not match the contracts, the 1099 process can bring those issues to the surface.

For growing businesses, the best time to review these details is before the year closes, not when the filing deadline is already approaching.

FAQs about 1099 reporting requirements

What are the 1099 reporting requirements for businesses in 2026?

1099 reporting requirements for certain payments to contractors, vendors, attorneys, platforms, and other recipients. The correct form depends on the payment type, recipient, amount, documentation, and IRS rules.

Does issuing a 1099 make someone an independent contractor?

No. A 1099 reports a payment. The IRS looks at the actual relationship, including control and independence, when reviewing whether a worker is an employee or independent contractor.

What is Form 1099-DA?

Form 1099-DA reports digital asset proceeds from broker transactions. It is relevant for digital asset sales and other broker-reported transactions covered by IRS rules.

Disclaimer

This article provides general information about Form 1099 reporting requirements, contractor classification, vendor payments, digital asset reporting, and business compliance. It does not provide tax, legal, accounting, or financial advice and does not create an attorney-client relationship. IRS rules, forms, deadlines, and guidance may change. Businesses should consult qualified tax and legal professionals before making reporting or compliance decisions.

Keep learning about tax compliance

To keep learning about business compliance in the United States, review Loigica’s resources on LLC structure, corporate compliance, contractor agreements, business immigration, tax-related documentation, and risk prevention.

1099 Compliance Review

Are your contractors, vendors, payments, and business records ready for 1099 reporting? Loigica can help review your structure, documentation, and compliance risks before filing season.